(This article was written in February 2022, with a slight update in May 2022.)

I. Introduction

In late 2021, Udi Wertheimer argued that Atomic needs a token.

tell them to reach out when they finally accept that they need a token

— udiverse (@udiWertheimer) December 30, 2021

Let’s first give Udi his due. Conventional wisdom says that new projects need new tokens. In the above Twitter thread, Udi simply applies that wisdom to Atomic. We appreciate Udi’s argument, and his humor. But we disagree. Although perhaps most projects do need their own tokens, Atomic doesn’t. The conventional wisdom doesn’t apply as clearly to us. You already know our answer (see Part I) In what follows, we explain why.

II. Token Benefits

Suppose you’ve built a new DeFi platform for borrowing and lending. You want people to use it, of course. But you also know that Field of Dreams is wrong: if you build it, they won’t simply come. Instead, you must lure people with incentives. So you create a new financial asset - a specialized token — that users receive as a reward.

As with fishing, some lures in DeFi are better than others. The more effective tokens in DeFi have better financial engineering—tokenomics, as it’s called. Several design choices factor into a project’s tokenomics, including:

- Total supply, or how many tokens currently exist

- Maximum supply, or how many tokens will ever exist

- Emission schedule, or how quickly total supply will reach maximum supply

- Emission constraints, or how people get new tokens

With the Cambrian explosion of new tokens, and the resulting competition among them, evolutionary forces have shown us which designs work better than others. The better the tokenomics, the more likely a project will have a growing and sticky user base.

More effectively designed tokens incentivize users to coordinate on a platform to help the platform provide a better service. If the token design offers a good reward, which draws more users, which leads to a better service, which draws more users, who then get more rewards, etc., the platform grows through a positive feedback loop.

Whether you think of altcoins as scams, distractions, or vehicles for acquiring more bitcoin, we must grapple with the science of tokenomics to appreciate Udi’s argument. And we can’t seriously engage his argument without knowing something about how some platforms create these positive feedback loops out in the wild. Along these lines, and outside of bitcoin world, Curve has, in my view, the most effective kind of tokenomics in DeFi. It has created such a flywheel for itself and its users that other platforms have begun to adopt its design with increasing frequency, much like an advantageous genetic mutation spreads through natural selection.

For full disclosure, I’ve used Curve, but I’ve never owned the Curve token. And now that I’m writing about it, I promise never to buy it. I’m not here to promote Curve but to discuss whether Atomic should have a token. And we can’t discuss this honestly without addressing whether Atomic should have what many have thought to be the most effective sort of tokenomics — Curve’s. In short, Curve is designed to pump like Hex but for an actual use case.

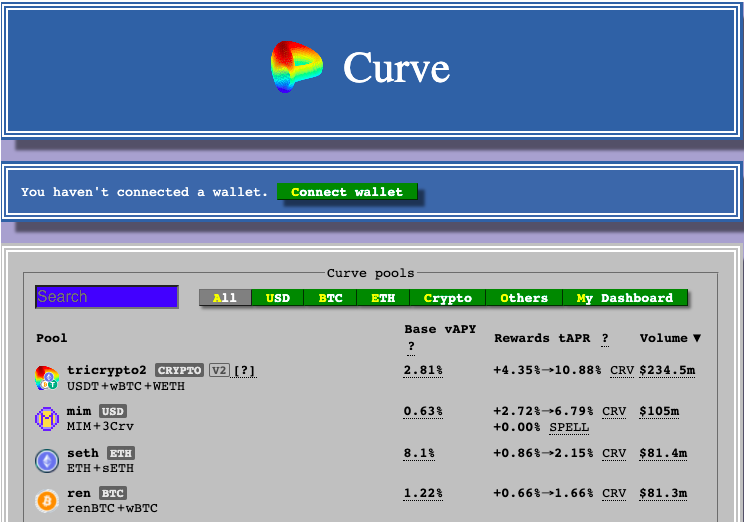

Before we address whether Atomic and its users would jointly benefit from issuing a Curve-like token, let’s first look a little more closely at Curve itself. Some quick background:

- The Curve platform allows users to swap similarly priced tokens for each other, like stablecoins for stablecoins.

- The platform offers extremely low slippage, i.e., users lose little value in the moment they trade one asset for another.

- Low slippage requires not only an effective algorithm but high liquidity, or high value amounts of the traded assets pooled on the platform. And Curve has both.

- Curve has high liquidity because users voluntarily pool their assets on the platform in exchange for a reward—the CRV token.

The more liquidity a user provides, the more CRV she gets. But users receive additional benefits for “locking” their CRV tokens on the platform. By locking CRV over longer time frames, a user receives two benefits:

- the ability to participate in governance and have partial control over the direction of the platform, including whether they get a bigger proportion of the CRV rewards, and

- boosted levels of CRV rewards.

These benefits incentivize people to pool liquidity with Curve, keep it there, and think twice about ever leaving. And the market’s knowledge about this design has second-order effects: those on the right-end of the bell-curve have good reason to believe the carrots will draw more liquidity and increase the CRV price, so they themselves pool more liquidity and buy more CRV. These rewards are so well-designed, in fact, that they overcome a user interface that looks designed by the creators of minesweeper.

Because of the evolutionary nature of the altcoin space, we’ll begin to see Curve’s model widely replicated. In fact, this replication has already begun with projects on alternative Layer 1s, bridges, Convex clones, and decentralized exchanges. This gives the chance for users who were late to Curve to be early in other similarly designed projects. So not only does greed push users into coordinating on a platform like Curve, it also draws waves of newcomers to pour their capital into newer platforms with Curve’s basic incentive design. This is beneficial for both the users and the new platform.

Could Atomic benefit from a Curve-like flywheel? We could give users the chance to be early on a token designed to pump and which lures the multitudes to come and stay. This could conceivably make Atomic a major coordination point for bitcoin yield and draw levels of liquidity and volume that would improve the user experience.

If we could create such a flywheel but don’t, then we’re vulnerable to a vampire attack. That is, someone could start a new platform with whatever software we open source, throw a Curve-like token on top of it, then siphon our users. In fact, Udi suspects we’re vulnerable to such an attack—by Udiverse himself.

well let me know when it’s ready maybe i’ll fork it and add a token

— udiverse (@udiWertheimer) December 30, 2021

To summarize, then, here are three potential reasons to create a token:

(1) incentivize users to come and stay

(2) decentralize the platform via governance

(3) prevent an Udi-led vampire attack

The first two are reasons for thinking that a token would greatly benefit Atomic. The third is a reason to think that Atomic wouldn’t survive without one. Is any of this true?

III. Incentives

Let's look at each of the three reasons for creating a token, beginning with the question of incentives.

Self-sovereignty vs. Pooled Liquidity

Bitcoiners seeking yield have limited options. Many fully surrender custody of their bitcoin for an IOU that the user can then use to generate yield through various DeFi legos on a smart contract layer 1 like Ethereum. This is what happens with WBTC: a bitcoin bank, BitGo, stores your bitcoin in exchange for a synthetic version on another chain. Many other users receive synthetic bitcoin through services like renBTC that offer an automated and more trust-minimized custodian.

Whether the entity wrapping your bitcoin is a smart contract or a bitcoin bank, the yield on wrapped bitcoin from various DeFi applications requires the user to sign off on a large subset of possible outcomes, not all of which can be known due to future contract upgrades. This is a tradeoff with EVM-style DeFi—you enjoy more flexibility with highly expressive smart contracts but at the cost of enlarging the attack surface. And attacks often succeed.

Many bitcoiners would prefer to earn yield on bitcoin without giving up custody and without making their holdings vulnerable to smart contracts with wider attack surfaces. This is possible, now, through discreet log contracts (DLCs). Each DLC spreads the entire contract logic over several off-chain bitcoin transactions. So DLCs need nothing more than bitcoin’s simpler and more secure script language. The attack surface is much smaller compared to EVM-style DeFi. But, as things now stand, DLCs do not enable users to enjoy a Curve-like flywheel.

With Curve and other platforms, users pool liquidity by depositing coins into a smart contract. In doing so, users sign for a large subset of possible outcomes, many of which cannot be known due to potential upgrades to the smart contract. This contrasts with Atomic, where the present state of DLCs on bitcoin requires that each user enters into a separate DLC with a market maker. As a result, users cannot usefully pool liquidity like they do with Curve.

At least for the foreseeable future, then, DLCs block part of a Curve-like feedback loop. Since Atomic has no pooled liquidity, creating a token wouldn’t draw users seeking the capital efficiency that arises from pooled liquidity. For now, a robust offering of bitcoin DLCs requires someone to handle the spread—the difference between bid and ask prices—and offer reasonably low slippage. And this is exactly what Atomic does.

Presently, then, users must weigh the tradeoff between earning a smaller yield through more secure DLCs and earning a yield juiced with altcoins through less secure EVM-style smart contracts. But let's not forget what often happens to altcoins with high yields. First, the more coins received, the less they're worth. Second, venture capitalists dump coins on ordinary retail investors, most of whom don't appreciate just how many coins the VCs acquired and for how cheaply. (Thanks, SEC!). Then, seasoned DeFi veterans know that these factors spell doom for the token and short it accordingly.

RIP.

Bitcoin has a decreasing and rigid supply schedule. And it has early adopters, not insiders, as my friend Andrew Bailey puts it. So yield on bitcoin, in bitcoin, is honest.

Bitcoin

— Cobie (@cobie) May 25, 2022

We think many will prefer honest yield in the best coin rather than a larger yield in down-only altcoins.

Simplicity vs. Revenue

Another segment of Curve’s flywheel consists of transaction fees. On Curve, users pay transaction fees that serve as revenue for CRV stakers. Should Atomic levy additional fees on users to pay holders of an Atomic token?

On the one hand, were we to levy additional fees and redistribute them as revenue to stakers of an Atomic token, users would simply pay more per transaction. And we want our users to pay as little as possible to earn yield on their bitcoin. We see little sense in making our platform expensive for the many for the benefit of the few.

On the other hand, we could provide discounted fees for Atomic token holders, implement a buy and/or burn mechanism, and so on, which together might put upward pressure on the token’s price. Conceivably, the token's appreciation might swamp any added transaction costs for users. But we don’t think altcoin revenue would outweigh the costs of making bitcoiners buy an altcoin to use our platform in the first place, especially since, as things stand, the token would need to operate with another protocol. We'll return to this point soon.

We’d rather maximize ease and simplicity for user experience.

Atomic Incentives

We can also add further incentives without an altcoin. Here are some incentives we’ve been considering.

Loyalty Points. We could offer a yield boost in the future to early users. Users might win a boost now that requires staying on the platform to enjoy. You can think of this as a kind of delayed “sats back” rebate. By using Atomic after having used it before, you win more sats.

Referral Programs. Users win sats for pulling others into our orbit.

Volume-based Discounts. Users who channel more volume through our DLCs enjoy smaller fees. Kraken offers similar discounts on trading.

Granted, none of these incentive programs offer the large yields we see in the wild west of DeFi. But bitcoin is not the wild west. It’s Venice. In any case, these programs together would incentivize users to come and stay, even as we offer the most secure, simple, and self-sovereign way to earn yield on bitcoin.

IV. Transparent Centralization

Atomic is committed to transparency, including where users encounter pockets of centralization. We have two main pockets of centralization — the reliance on oracles for settling DLCs, and the app itself, which relies on the team’s development and our specialized knowledge in creating things like back-tested recurring strategies. These are, right now, inevitable pockets of centralization for creating DLC-sourced bitcoin yield. We refuse to hide behind a governance token as if these pockets of centralization do not exist.

Furthermore, a governance token is completely unnecessary for Atomic. CRV’s token provides voting rights for directing CRV rewards to different liquidity pools. But we have no liquidity pools, no token to incentivize them, and so nothing to vote on about how to incentivize them. Furthermore, bitcoin could itself serve as a governance token. Atomic users could use their private keys to sign votes in a poll, and we could weigh votes according to bitcoin held.

V. More Issues with Tokens

Regulatory Concern

Issuing a token isn’t risk free. Regulators and law enforcement know who we are—or, at least, could easily find our identities. Atomic calls Canada home, and the regulatory picture in Canada has recently become less clear.

On the one hand, Atomic doesn’t take custody of any user's bitcoin, thanks to the structure of DLCs. So no user needs to worry about having their bitcoin censored or confiscated through Atomic. On the other hand, tokens look like securities, especially when they have an accompanying foundation or development team—like we do. Since we seek to abide by the law of the land and behave honestly, we would rather not offer a security under another name.

Distraction

We must optimize for improving our core products. Although we have a highly productive team, we are still admittedly small. So a new token would distract and delay. An Atomic token would not only need to overcome the problems above, we’d have to decide how the token would work, how we would distribute it, and whether it would primarily inhabit bitcoin layer 1 (through colored coins, like Bisq’s token), Liquid, Lightning, or some other network entirely (like Bitfinex’s LEO token). Then, we’d have to decide the best implementation for whether the token and our DLCs should settle to the same network. We're still incredibly early, too, with potentially game-changing developments on the horizon. Settling these questions now feels like aiming for a moving target.

These questions don't admit of easy answers. Right now, we can best use our energy and brainpower on improving the product and enhancing the experience for our users. With our focus on what matters most, everyone will soon be able to leverage the magic of DLCs and earn bitcoin yield privately and in a self-sovereign way.

VI. Conclusion

We could be wrong about needing a token. Or we could be momentarily correct, only for the situation to change later. Either way, we would have time to pivot and stave off a vampire attack. If the situation changes enough that we can issue a token to the great benefit of our users and without sacrificing our ideals, we could issue a retroactive airdrop for those who have used our platform — a la Uniswap. We probably won’t. But we could. And if we ever did, we'd do it fairly and without unduly rewarding ourselves.

But, again, we doubt this will be necessary or wise. First, the DeFi DEX aggregator Matcha has done well, beating many decentralized exchanges and aggregators without having a token. Second, we expect that altcoin incentives can unwind quickly, as token prices lose value, leaving platforms worse off than they would have been without any token at all.

So Vampire attack us if you wish. We welcome the competition. In the meantime, we will optimize our main offerings and work to offer the most secure, beautiful, and private avenue for bitcoin yield.

Join the Sound Finance Movement

Atomic Finance builds sound finance products for sound money.

Our first Sound Finance product is a mobile app that provides self-sovereign Bitcoiners a way to earn a return on their bitcoin with full transparency. Without having to give up custody of their coins to a third-party custodian.